Holman Jenkins had an excellent editorial at the Wall Street Journal on Wednesday with a timely reminder of the several ways in which the Consumer Financial Protection Bureau, created by Dodd-Frank in 2010, is basically a rogue agency in the U.S. federal government.

The reminder is timely, of course, because of the attempt by the CFPB’s departing director, Richard Cordray, to outmaneuver the president and prevent him from gaining influence over the Bureau’s operations by installing the new chief.

Jenkins calls this, effectively, a coup attempt (his word). And he’s not wrong. The CFPB was designed by the Democrats in Congress – who controlled the body when Dodd-Frank was passed – to escape accountability to either the legislative or executive branch. The Bureau is funded through the Federal Reserve, and so does not depend on an allocation from Congress.

The Dodd-Frank language for appointment of new CFPB directors conflicts with the federal Vacancies Act of 1998 (the basis for the unfolding confrontation with President Trump), and was intended to insulate the CFPB from future presidents who might not have the left-wing activist perspective of Barack Obama, or of the Bureau’s chief proponent, Elizabeth Warren..

An alerted public, at least on the conservative end, is largely aware of these points as the current week crests its hump. But Jenkins reminds us that the CFPB also engages in the Obama-era practice of using shakedown fines (“civil penalties”), levied in this case on lenders, to enrich left-wing activist organizations.

Made-up “evidence” of bad lending practices

It’s worth reviewing the basis on which those fines are imposed. Here is Jenkins:

Recall that one of the new agency’s first priorities under Mr. Cordray was to go after auto dealers, though Dodd-Frank explicitly excluded them from the agency’s oversight.

Recall that he sought not to regulate their disclosures but to ban a practice that he and other activists decided they didn’t like, namely dealer-negotiated interest rates on car loans, though the agency had no authority to do so. …

Because he can’t regulate auto dealers, he targeted banks that finance auto dealers. Because auto dealers are forbidden from collecting racial data on borrowers, the upstream lenders can’t know the race of borrowers. Yet Mr. Cordray charged them with disparate impact based on so-called Bayesian Improved Surname Geocoding, which assigns borrowers to a racial category based on their names and zip codes, though the method is not designed for such purposes and known greatly to overestimate the number of African-Americans in the U.S. car-buying population.

Even this does not do justice to the disingenuousness of the agency’s method. Any person identified as having a black-sounding name who paid a higher rate than the average of people with white-sounding names was deemed to have been a victim of discrimination, never mind that many people with white-sounding names also paid a higher rate. …

By such means the agency fabricated—there is no other word—evidence of racial disparity in auto lending to shake money out of lenders, without effective court appeal, because the agency was able to hold necessary approvals the banks sought from other federal agencies hostage until the banks settled.

Jenkins published a column in 2014 with more detail on this tortured method of “evidence” fabrication.

But he also closes his discussion of the auto-dealer example with this nugget:

That’s not all: Part of the proceeds were then distributed to activist groups that supported the CFPB’s creation and mission.

Shakedown payouts to political allies

Ah, yes. Government agencies as dispensers of shakedown proceeds to favored political allies. The Obama administration plowed new ground in that regard, as previously outlined in LU posts (additional examples linked from this one).

The CFPB has published few details that would give insight on this, so we must hope that Mick Mulvaney, Trump’s newly appointed director, will increase the Bureau’s transparency. But we do have some glimpses from the past few years of what’s been going on.

In 2014, the General Accounting Office (GAO) published a report on the CFPB’s Civil Penalty Fund in response to a request from House Republican Shelley Moore Capito . Keep in mind, the CFPB collects fines for “redress” – direct payment to victims – and as a separate matter levies the “civil penalties,” which it can then allocate to its taste.

What the GAO had found was summarized at this site (emphasis added):

The report indicates that as of May 30, 2014, the CFPB had collected more than $139 million in civil penalties and allocated over $31 million to compensate seven classes of harmed victims. It also made one allocation of $13.4 million for consumer education and financial literacy programs, with funds in such allocations designated for a program that provides financial coaching for transitioning veterans and economically vulnerable consumers. (Based on the numbers shown in the report, which include a set-aside of approximately $1.5 million for administrative expenses to administer payments to victims, the CPF had more than $93 million in unallocated funds as of May 30, 2014.)

The bolded allocation is the one made to activist groups. We’ll look at who those are and how they are selected in a moment.

In 2015, an update posted in the FAQ section at the CFPB website showed a second allocation “for consumer education and financial literacy programs” of $15.4 million. Again, these are the allocations going to activist organizations.

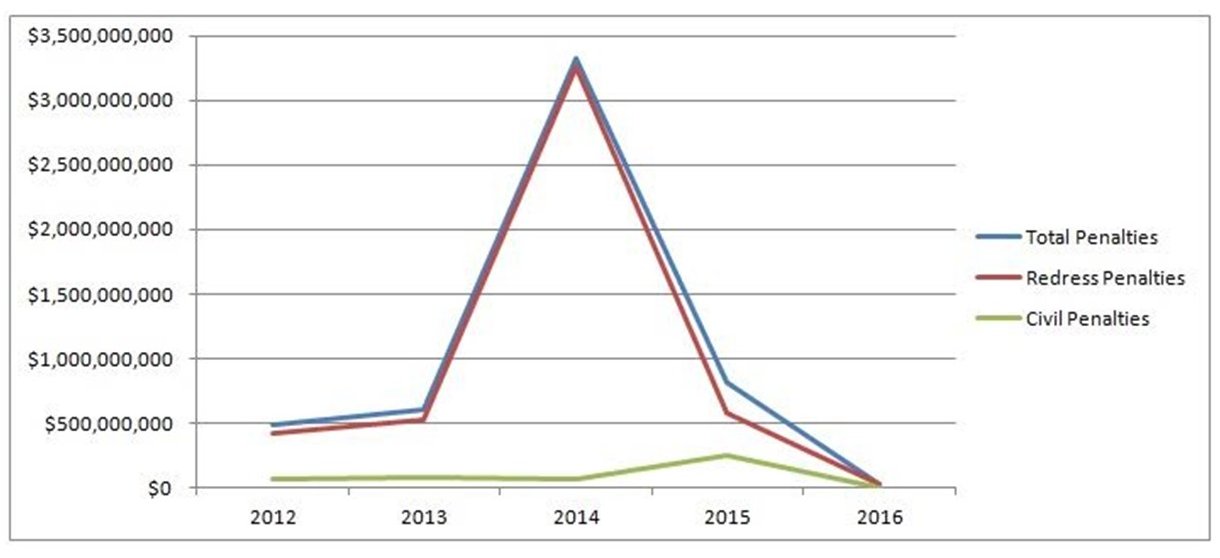

They seem to represent only a small percentage so far of the total take in the Civil Penalty Fund. This summary from an industry website in 2016 has some crude data on the total CFPB assessments in civil penalties, as opposed to strict victim-redress penalties, since 2012. Although civil penalties are a relatively small percentage of all CFPB assessments, the total of all assessments from 2012 to early 2016 was over $5 billion, and in 2015, civil penalties alone topped $200 million.

$29 million of that has been disbursed in allocations to activists; we are justified in wondering what is happening with the rest.

The GAO report of 2014 expressed the following reservations:

The GAO found that the CFPB failed to document the factors that the CFP administrator considered in deciding to allocate $13.4 million for consumer education and financial literacy programs. While the report indicates that the CFPB had revised its procedures for administering the CPF to include the factors the administrator will consider when determining such allocations, the GAO found that, at the time of its audit, the revised procedures did not include steps for the administrator to document the specific factors that were considered as part of an allocation.

According to the GAO, the CFPB agreed that it should write up the factors it would consider for allocating Civil Penalty Funds to activist groups. It has done so here; however, there is no obvious mechanism for verifying how fund recipients meet the criteria outlined by the CFPB (some of which are, in any case, subjective).

Who are the political allies getting the payouts?

In 2015, Investor’s Business Daily was able to obtain a list of activist groups designated for civil penalty allocations by Richard Cordray (along with then-Labor Secretary Thomas Perez). Only a few groups are listed by name here, but IBD has the following:

[T]he agency will bankroll some 60 liberal nonprofits, many of whom are radical Acorn-style pressure groups. It says these organizations will provide “financial coaching” for low-income homebuyers, as well as “housing and social services.”

But their activities are more political than charitable. IBD obtained a list of groups eligible for the bank payola, as approved by CFPB Director Richard Cordray and Labor Secretary Thomas Perez. It includes:

-

The Legal Aid Society of the District of Columbia, whose directors include senior Democratic National Committee officials; the self-described “policy advocacy” group has lobbied Congress for more welfare spending at least 108 times since Obama took office.

-

The Mississippi Center for Justice, whose stated mission is “advancing racial and economic justice” and “attacking predatory lending practices.”

-

People’s Community Action Corp. of St. Louis, which has seated Obama appointees and Democrat lawmakers on its board.

The deciders-in-chief (and how they roll)

How do the recipients get designated? According to the CFPB website, the decisions are made by a Civil Penalty Fund Governance Board. Its composition is described as follows:

The Civil Penalty Fund Governance Board is chaired by the Bureau’s Chief of Staff and includes the Associate Director for Supervision, Enforcement, Fair Lending & Equal Opportunity; the Associate Director for Consumer Education & Engagement; the Chief Operating Officer; and the General Counsel.

The board is thus composed entirely of CFPB staff members. That in itself ought to be a red flag, especially since there is no effective oversight of the CFPB. For general drill, we can take a look as well at who the incumbents are on this board:

Chief of Staff – Vacant; was Leandra English until Richard Cordray appointed her as his deputy a few days ago, in the attempt to make her his successor instead of Trump’s appointee.

Associate Director for Supervision, Enforcement, Fair Lending & Equal Opportunity – Christopher D’Angelo. With the Bureau since 2011, having come over from a topically related job in domestic financial regulation at Treasury (where the CFPB was birthed). Served as a senior adviser to Richard Cordray from 2012 to 2013, and then as chief of staff(Leandra English’s old job) until 2016. When he was appointed to his current post in 2016, the move was criticized in some quarters as one of political favoritism, based on his connection with Cordray.

Without attempting to assess that aspect of it, we can say that D’Angelo’s links to Cordray and positions held at the CFPB suggest he would vote as Cordray would on board decisions about civil penalty allocations.

Associate Director for Consumer Education & Engagement – Gail Hillebrand. Long-time activist; formerly a senior official of the Consumers Union (publisher of Consumer Reports), and founder in the late 1980s of the California Reinvestment Committee (now the California Reinvestment Coalition), one of the legal activist groups that used the Community Reinvestment Act of 1977 to pressure mortgage lenders into making risky loans – and handing over millions in loan monies to be managed as “special funds” by community-activist organizations. Also with the CFPB since 2011.

Chief Operating Officer – Sartaj Alag. A rare senior executive who came from industry (Capital One, with a prior background in management consulting and an engineering degree), Alag was with the CFPB from the beginning (in 2011), but departed and then returned in 2013 to take the COO position.

In his stint in the early days of the CFPB, Alag had a special relationship with agency patron Elizabeth Warren, as described in 2014 by the Washington Post:

Many of the culture efforts were driven by Sartaj Alag, the former head of Capital One in Canada who came on as an adviser to Warren, supplying her with advice from management philosophy books like “Good to Great” and “Level 5 Leadership” (he’s now chief operating officer at the bureau). Early on, he organized a survey of the staff to come up with the CFPB’s official mission and vision.

The Post piece from 2014 is worth a few more quotes, because it highlights how the CFPB was launched as basically a federally-funded ACORN-type outfit, full of beans and determined to push the envelope of possibilities regarding its mission and operating profile. Alag was one of several “present at the creation” members who took to this vigorously.

“They started out with such a complete rethinking of everything,” said Jo Ann Barefoot, a former deputy comptroller of the currency who tracks the CFPB for a financial services consultancy. “I think they were more clear on what they were not than what they were.”

(Note: Ms. Barefoot was on the CFPB Consumer Advisory Board in 2015.)

Emphasis added here:

Officials tasked with the [CFPB] setup had little…guidance. Consultants provided them with a binder of case studies on how other agencies had been launched. But most of these were either bad examples, such as the Department of Homeland Security’s disintegration into feuding fiefdoms, or not applicable. Even the Securities and Exchange Commission, built in the aftermath of the Great Depression, didn’t have the immense range of mandates granted to the Bureau.[Yet there was little guidance for the CFPB’s setup. Government at its finest. – J.E.]

In particular, the binder was silent on how to hire people. Applications poured in from idealistic young lawyers, and Warren — then a special adviser to the Treasury and the CFPB’s de facto leader — brought on recruits from Harvard. The bureau’s headhunters especially liked passionate applicants who had some personal experience with the financial crisis — somebody they knew lost a house or job — and an intense devotion to the agency’s mission.

The “start-up” phase was thrilling because it was like a small business start-up.

Soon the ballooning staff expanded into government space in a nondescript office building. New recruits would show up to no desk, no phone and way too much to do. All-hands meetings were held in the elevator lobby, with people sitting on the floor while Warren gave pep talks. Even senior hires often started out in a big, windowless room called “the cave.” But the bureau had lured the kind of people who wouldn’t mind all that much.

“It didn’t faze me at all, because I was an entrepreneur. It just brought me to the first day of my company, where we’re all on picnic tables in an attic,” said Pete Carroll, who became assistant director for mortgage markets. “It turned out to be the nerve center. Someone said, ‘Do you want to move?’ I said, ‘No, this is great! Everybody’s buzzing around, Elizabeth Warren’s popping her head in.’ I was like, ‘this is awesome, this is the greatest thing ever.’”

Sanity break: this exciting, lobby-meeting start-up agency full of passionate, one-issue people was insulated from congressional oversight, had a bigger charter of mandates than the SEC, and would have the power to drag lenders through the courts, making you, the creditworthy public, pay higher interest rates and fees to those lenders so that the CFPB could assess “civil penalties” and allocate money to the recipients of its choosing.*

I don’t think there can be much doubt about how board member Sartaj Alag would vote on allocating civil penalty payouts. (Meanwhile, for me, Trump’s determination to rein this agency in, and perhaps do away with it, is looking pretty good. We can – and should – do better.)

General Counsel – Mary McLeod. Ms. McLeod took her position in late 2015, coming from a career in the State Department and no background in consumer finance. Not surprisingly, perhaps, she wrote an official opinion for the CFPB on 25 November that Donald Trump’s authority to name Richard Cordray’s successor is the controlling factor. That opinion accords with what every judge who sees the suit brought by Leandra English (through the funding of anonymous donors) is virtually certain to rule.

Given her background, McLeod might exert some balancing influence on the Civil Penalty Fund Governance Board – although there is no accountability or enforcement mechanism to give her opinion weight.

One other key thing the CFPB had the power to decide – until Trump stepped in

In July 2017, the CFPB issued a rule that lenders cannot enforce binding arbitration clauses to settle disputes with borrowers out of court. (LU contributor Edward Woodson addressed it at the time.)

As CFPB noted, many lenders had such clauses in their contracts with borrowers (e.g., credit card holders and loan borrowers). The CFPB’s intent was to override those clauses and ensure that all lenders could be pursued in court.

The Republican Congress and Trump voided that rule on 1 November 2017, which CFPB now notes in its online copy of the original announcement.

The CFPB listed three justifications for its July 2017 rule. Of those, the one quoted below is the one that matters. If lenders can close disputes with arbitration, the cost of resolving those disputes is less.

What the CFPB doesn’t point out, but what is glaringly obvious, is that cases closed with arbitration don’t make any money for the CFPB Civil Penalty Fund.

- [Lenders can] Avoid paying out big refunds: Individual actions get less overall relief for consumers than group lawsuits because companies do not have to provide relief to everyone harmed. According to the study, group lawsuits succeed in bringing hundreds of millions of dollars in relief to millions of consumers each year. The study showed that over 34 million consumers received payments, and that $1 billion was paid out to harmed consumers over the five-year period studied. Conversely, in the roughly one thousand cases in the two years that were studied, arbitrators awarded a combined total of about $360,000 in relief to 78 consumers.

* You do understand, I am sure, that lenders don’t pay civil or redress penalties. Their solvent, payment-making customers pay the penalties. The lenders have nothing to pay penalties with except the revenues they collect from lending to the solvent.

Crossposted With Liberty Unyielding